The international banking system is struggling to maintain its relevance. With international transactions taking days and even weeks to happen, it makes a mockery of the digital age. Let me give you my own personal experience.

I live in Sydney, Australia, and still have a bank account in the UK. As it stands right now, it is quicker for me to

- fly from Sydney to Heathrow,

- drive down to Brighton on the South Coast where my UK bank account is based,

- pick up my cash,

- go onto Brighton’s pier and get my kiss-me-quick hat and Britain's contribution to haute cuisine - fish and chips before travelling back to Heathrow and flying back to Sydney

than it is to transfer my funds from the UK to Australia via the traditional banking system.

At a time when millennials think today is already too late, the banking system just shows a disconnect to the needs of those who are digitally native - which helps explain the ever-continued success of so many Neo-banks.

There are new financing models, however, that continue to be developed that are primed and ready to disrupt capital markets globally, embracing the digitally native. These disruptive forces have evolved organically over the past 13 years and are based around the power of Blockchain technology, the immutable and irreversible powerhouse, that underpins Bitcoin.

In this article, we will explore how fractional funding based on Blockchain technology has the power to prise open up global banking and investment markets with technology that defines digital ownership and enables near-immediate international transactions

The Blockchain - banking re-visited

The Blockchain started its commercial journey in January 2009. Right from the get-go, the writing was written loud and clear on the hallowed walls of the banks with the first line of the abstract of Bitcoin's whitepaper summarising it best:

“A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution.” Bitcoin Whitepaper

The initial power of Bitcoin, which has spawned so many other cryptocurrencies, was to transfer international payments almost instantaneously via a new set of payment rails.

Smart Contracts - the programmability of money

- You insert your cash,

- You choose your sweeties and

- You pick them up from the dispensing tray.

All the computer work goes on behind the scenes, and, in very simple terms a contract is established

- The vending machine offers the opportunity to buy the sweeties,

- You accept by agreeing to buy them, and

- Consideration is made when you insert your funds.

All the calculations go on within the vending machine itself.

This same structure was deployed in 2016 when the Commonwealth Bank of Australia and Wells Fargo undertook an international transaction using smart contracts for the shipment of cotton from Australia to China.

- As the ship passed into Chinese waters, it triggered a GPS sensor on the container.

- The GPS sensor sent a signal to the cloud that triggered a smart contract

- This smart contract automatically released funds to the cotton seller based on the GPS data and the smart contract that programmed the details of the sales contract between buyer and seller.

This transaction was the first to test and replace the heavy paper-oriented process that Banks used for international transactions (via Letters of Ccredit).

Using smart contracts all digital transactions have the capbitlity of being programmed, with this enabling Initial Coin Offerings (ICOs).

ICOs - the beginning of fractional funding

ICOs were prevalent in 2016 and 2017 and represented crowdfunding on steroids. A new blockchain platform would be designed by a team and funded by crowdfunding the software tokens, essentially cryptocurrencies, used to power the platform being developed. The power of ICO’s came from the ability to move these tokens between international cryptocurrency exchanges almost instantaneously.

ICOs were highly successful, raising $24 billion of global capital - over 20% of the US venture capital market in 2017 using a technology that had been around for only 12 months. Critically, none of this capital went through the traditional banking system.

ICOs opened up the world of democratic capital, where funds from anywhere could easily and cheaply be transferred globally to support projects. There was a major difference, however, that had regulators on the back foot.

Unlike the dot com boom and bust before it, the ICO boom was powered predominantly by individuals, rather than institutional funds. Those that backed the blockchain projects truly understood the technology and goals of the platforms being funded, and in most cases understood the projects were high risk. Perhaps most importantly, it was also the first real taste of where the internet itself embedded financial value by using blockchain technology without needign to enter the external banking system. ICOs laid the foundation for the transformation from the internet of information to the internet of value. It was further enhanced by the blockchain being able to define digital ownership.

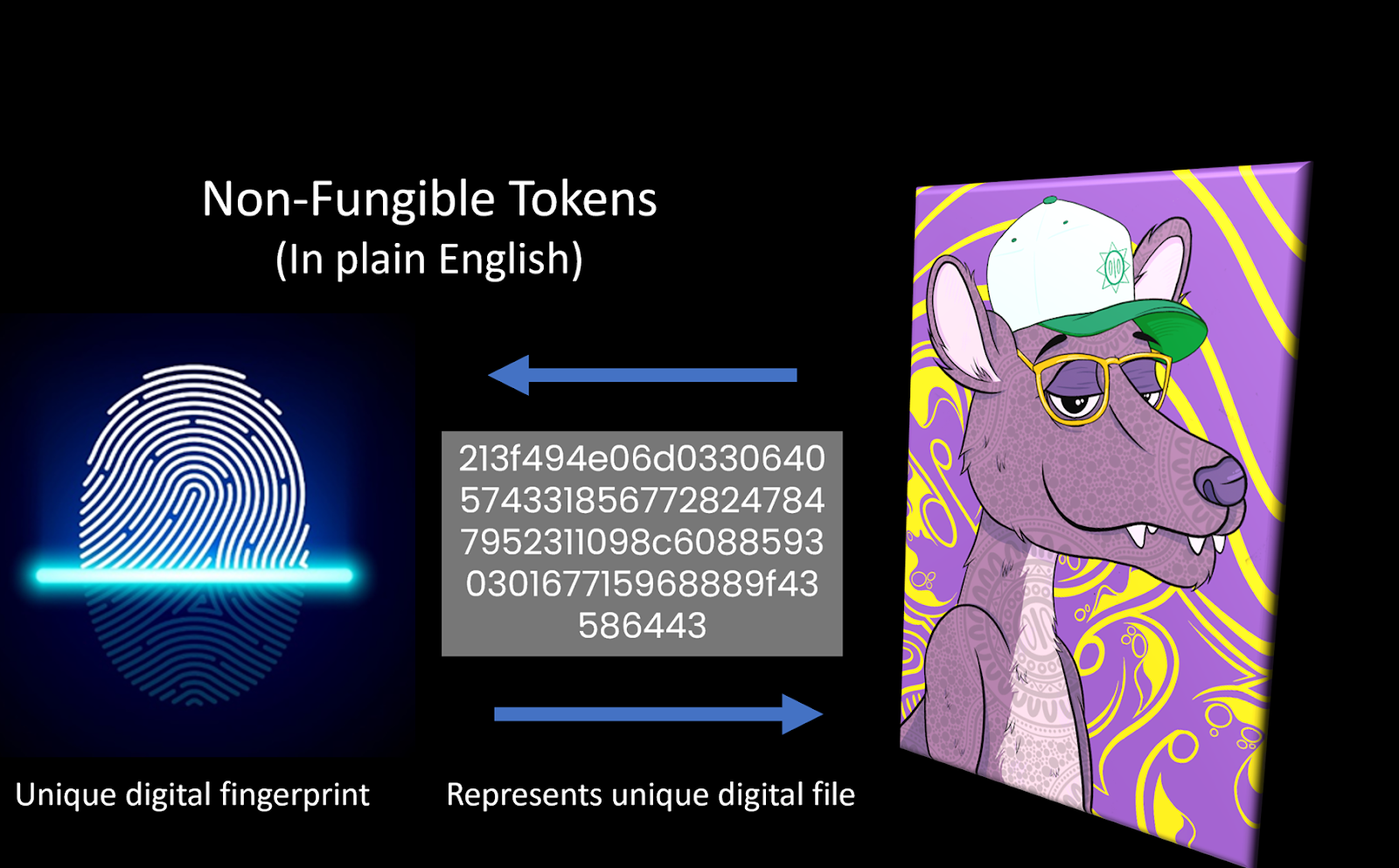

NFTs (Non-fungible tokens) - defining digital ownership

The Power of NFTs, smart contract to provide Fractional Ownership

The fractional ownership of assets is not a new idea. In the real estate market, Real Estate Investment Trusts (REITs) are an established funding structure, globally. Equally, many vertical markets already have fractional ownership models – e.g. shared ownership of racehorses, boats, timeshares etc. Let’s extend this to the digital realm

Given NFTs represent digital ownership of a digital file via a unique digital fingerprint, imagine breaking that digital file up into individual pieces - eg pixels of an image or frames for a video - and defining ownership of those individual pieces via NFTs.

Where this becomes really powerful is the ability to trade those NFTs, that are almost identical in structure to cryptocurrencies. It means these fractional NFTs can be moved globally and near instantaneously at negligible cost. This creates a multitude of new opportunities.

This concept of converting economic rights associated with assets into digital tokens is called tokenistion. These tokens can be programmed and stored as a permanent record on a Blockchain and subsequently transferred from one party to another. Almost any asset and its associated economic rights can theoretically be tokenised and traded.

One example that showcases where this technology has been used to fractionalise assets was with a project called fractional.art. They established the idea of being able to own fractions of the major blue chip NFTs such as the infamous Bored Ape Yacht Club collection. The ownership of each NFT was broken down into portions of the original NFT. The biggest challenge is that as Forbes highlighted the SEC, the US regulator, was looking very carefully at fractional NFTs. Whether the issues are related or not, or because the NFT market has collapsed by around 85% in line with the crypto winter, the fractionalisation of Fractional art’s NFTs is being disabled in the future . The model has been tested and in so many ways proven to work.

Fractional ownership of Physical Assets

The structure of fractional ownership can, in theory at least, be extended to include fractional ownership in almost any identifiable physical asset – property, a solar farm or pieces of art. If for example the deeds to a property, as a digital word document that can be uniquely identified, could be tokenised and divided into 100 NFTs - each NFT would represent 1% of the ownership of the property - imagine how powerful that could be. Of course, some caution does need to be seen - especially in regards the governance of the physical asset. In other words who administers the decision-making process to sell the asset and under what circumstances.

On the positive side, an investor could buy 1% of a flat in Berlin, 2% of an apartment in New York and 1% of a holiday home in Sydney. Long gone would be the problem of digital natives getting on to the property market. Just imagine how this would affect markets in terms of additional liquidity, globally. It would enable historically highly illiquid markets to be better defined, making markets more efficient over time as price discovery is enhanced.

The challenge for any fractional funding, however, is that regulation has to catch up with the technology.

The Balancing Act of Regulation

Sadly, regulation always lags behind technology. This is not because regulators don’t want to embrace new technologies but because regulators can only regulate what the lawmakers put into law, i.e. governments. When we consider the average age of US congressmen and women is 58.4 years and senators 64.3years, the majority of the lawmakers have not grown up with technology all their lives. As a result, there will be a natural lag in their own knowledge. With that lack of understanding of the latest technologies, comes the lack of understanding of the risks. Education will help, but it will be a very slow process. So, regulators have to work within the current legal structures that exist.

Fractional ownership from the regulator’s perspective falls under today’s laws. These are defined by different definitions globally but include for example, Collective Investment Vehicles, Manged Investment Schemes or Real Estate Investment Trusts (REITs). New projects are typically shoehorned into existing legal structures or, in the worst cases, enforcement actions implemented leveraging existing legislation.

Industry associations are very aware of the regulatory challenges and are seeking to implement best practices that professional members should follow. Whilst there is no guarantee that enforcement action won’t follow, by creating a professional landscape for the professional development of innovative ideas, regulators can see the efforts being made to reduce the incidence of bad actors. Naturally, this is an iterative process that will be ongoing, frustrating as that may be.

An idea for the future

Fractional ownership makes sense for anyone that has experienced how easy it is to programme and move funds internationally using cryptocurrencies. Yet, regulations do not embrace this same power with the same relish, which presents a some inconsistencies, with an individual’s right to discretion of how they spend their own funds.

Across the globe, the majority of casinos around the world allow anyone over the age of 18 the ability and right to gamble essentially as much as they wish. Equally at the racecourse if you are over 18 years old you can gamble as much as you like. Yet individuals do not have the discretionary right to invest even $100 in Pre-IPOs or to invest in pre-ICO cryptocurrencies for example, unless they are accredited investors. This presents a massive disconnect between the technology users, that understand the technology and most of the risks, and the regulation needed to frame it legally. As a result, technology tends to be squeezed into a box that relates to historical precedents from the dim and distant past. Of course, no-one wants to see consumers being ripped off by inappropriate projects - we have seen too many of those already. So here’s an idea for exploration.

It makes common sense for individuals to have the discretion to spend or invest their funds how they seem fit. That said, regulators need some form of control mechanism to be in place. So, how about regulators providing some discretion to non-accredited investors by establishing a licencing structure for those that wish to participate and for those that want to be able to invest in fractional ownership?

-

A licence is offered based on online education to showcase the risks and to provide understanding to potential investors

-

Results are locked to a blockchain linked to the identity of the participant

-

The participant can invest in approved projects curated by trusted parties, which links to the investor’s identity

-

Different levels of licencing are made available to different parties according to how much education they have undertaken.

-

The smart contracts of a project can automatically stop any investment beyond the investor’s licenced level.

Conclusion

Fractional ownership has some exceptional power and when you first embrace it you get a great sense of excitement. Like all new technologies, however, it takes time for regulators to catch up to where the technology is heading and to regulate the risks that the lawmakers determine need to be regulated. In the technology space, there is an expression that rings so often in entrepreneurs' ears - “ask for forgiveness, not permission”. In fintech, as we all know too well, unfortunately it doesn’t work well and can end in tears.

So all we need is patience to see regulators and lawmakers to catch up to the power of the new technology and sadly, that could take time - probably a very long time.